249% Returns with 82% Less Volatility - Research Article #61

How a Systematic Momentum Strategy Delivers Steady Growth in Crypto's Wild Market

👋 Hey there, Pedma here! Welcome to the 🔒 exclusive subscriber edition 🔒 of Trading Research Hub’s Newsletter. Each week, I release a new research article with a trading strategy, its code, and much more.

If you’re not a subscriber, here’s what you missed this past month so far:

If you’re not yet a part of our community, subscribe to stay updated with these more of these posts, and to access all our content.

Introduction

In the high-stakes arena of cryptocurrency trading, the allure of extraordinary returns often masks a sobering reality:

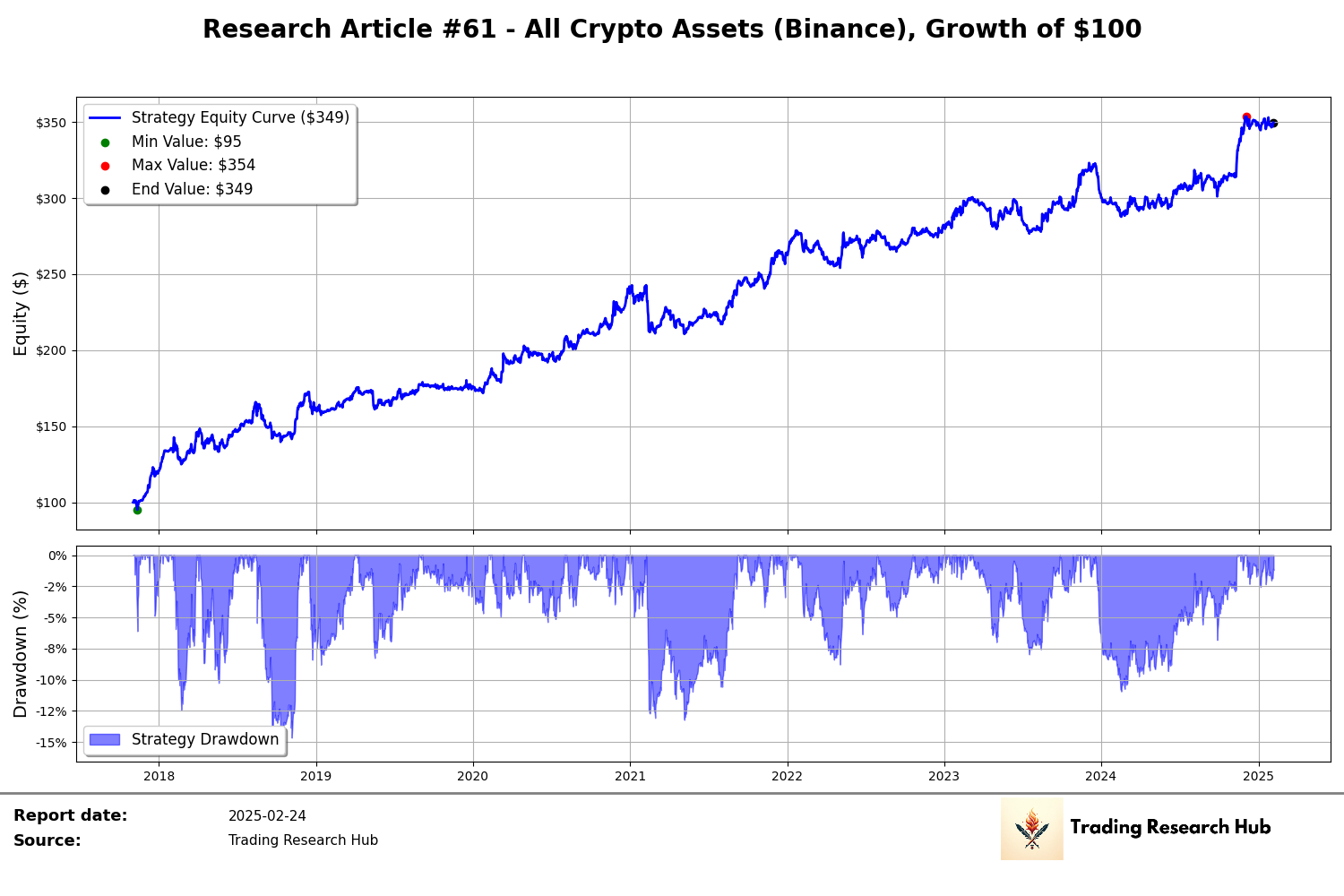

Extreme maximum drawdowns of over 90% and severe volatility exceeding 80% have become standard occurrences rather than unusual events.

Yet amidst this chaos, this systematic approach has demonstrated that it's possible to capture significant upside while maintaining drawdowns controlled (<16%) - an accomplishment that challenges conventional crypto trading wisdom.

The performance metrics tell a compelling story: while the broader market whipsaws traders with extreme volatility, this strategy achieved a Sharpe Ratio of 1.25 - significantly outperforming both benchmark and market indices (0.91 and 0.92 respectively).

This isn't merely about risk reduction; it's about intelligent risk deployment. By maintaining strategic long-short exposure, and by doing so reducing annualized volatility to just 14.67%, the approach has delivered consistent returns while allowing traders to sleep better at night.

These results emerge from a deep analysis of market behavior that reveals fascinating patterns: large, liquid cryptocurrencies exhibit distinct momentum effects over 1-2 week periods, while smaller, illiquid tokens display significant reversal characteristics.

The data demonstrates that high-momentum strategies can generate substantial profits while maintaining strict risk parameters - achieving a remarkable return-to-drawdown ratio of 65.90 compared to the benchmark's 36.24.

In the following sections, we'll deconstruct the precise methodology that enables these results.

Table of Contents

Introduction

Strategy Thesis

Data and Methodology

Performance Analysis

Conclusion

Strategy Thesis

The core thesis is that momentum strategies can generate positive returns in the short term due to the persistence of price trends, market inefficiencies, and the unique characteristics of cryptocurrencies.

Supporting Evidence for Momentum Strategies

Short-Term Momentum Effects:

Research has identified significant short-term momentum effects in cryptocurrency markets. Assets that perform well over a specific period (e.g., 30 days) tend to continue outperforming over the subsequent short-term horizon (e.g., 7 days). Long-only momentum trading strategies that exploit this phenomenon have consistently delivered excess returns relative to benchmarks like Bitcoin (Antonakakis et al., 2023).

Profitability of Long-Only Momentum Strategies:

Long-only momentum strategies, which focus on buying top-performing cryptocurrencies while avoiding underperformers, have consistently delivered excess returns. These strategies leverage the continuation of positive trends in digital assets (Antonakakis et al., 2023).