1,127% Return with 67% Less Volatility - Research Article #62

Your exposures should be dictated by you, not the market...

👋 Hey there, Pedma here! Welcome to the 🔒 exclusive subscriber edition 🔒 of Trading Research Hub’s Newsletter. Each week, I release a new research article with a trading strategy, its code, and much more.

If you’re not a subscriber, here’s what you missed this past month so far:

If you’re not yet a part of our community, subscribe to stay updated with these more of these posts, and to access all our content.

It was the 31st of December 2023, when I was holding one of my largest single winning trades to date.

At the peak, I had an open return of over 400% of my initial position. But I made a discretionary decision, that ended up being the best decision to make at that time…

I entered $TRB at $103.91, a few weeks prior to the massive move as the coin was gaining momentum.

It’s business as usual until the coin passes over the $200 mark, and things start to accelerate exponentially.

Now my position is growing 20%, 30%, a day.

The problem of having a position that is up 150% in a few weeks, is that any small intraday movement leads to significant volatility to our portfolio.

On its final day, the coin went up almost 150%.

My position was massive at that point, compared to what I usually hold.

So I thought:

“Given that the volatility is extreme, and I am holding a substantial amount on an asset that is up 400% in a few weeks, holding it blindly might not be the wisest decision.”

And this is one of the rare occasions where I intervened, went against my system, and rebalanced my position back to a target weight that I deemed acceptable.

I got lucky and ended up closing a large chunk of that position at the top.

This taught me an important lesson, despite only realizing its importance at a later date:

You should only accept exposures that you want, and not those that the market forces to you.

It is fun to ride massive positions on the way up, but had I held it as originally planned, I’d have given back a total of 70% of the peak returns of that trade, in a single day!!

This is what we will be examining today.

Despite taking that decision discretionarily, we can turn it into a systematic approach to trade.

In general, we want to have exposures that we believe we should have, not that the market forces into our book.

Rebalancing positions into target weights, when they become either too large or too small, should keep our equity smoother, by reducing that uncontrolled volatility we allow when we ONLY close positions at the exit.

But how does that apply practically?

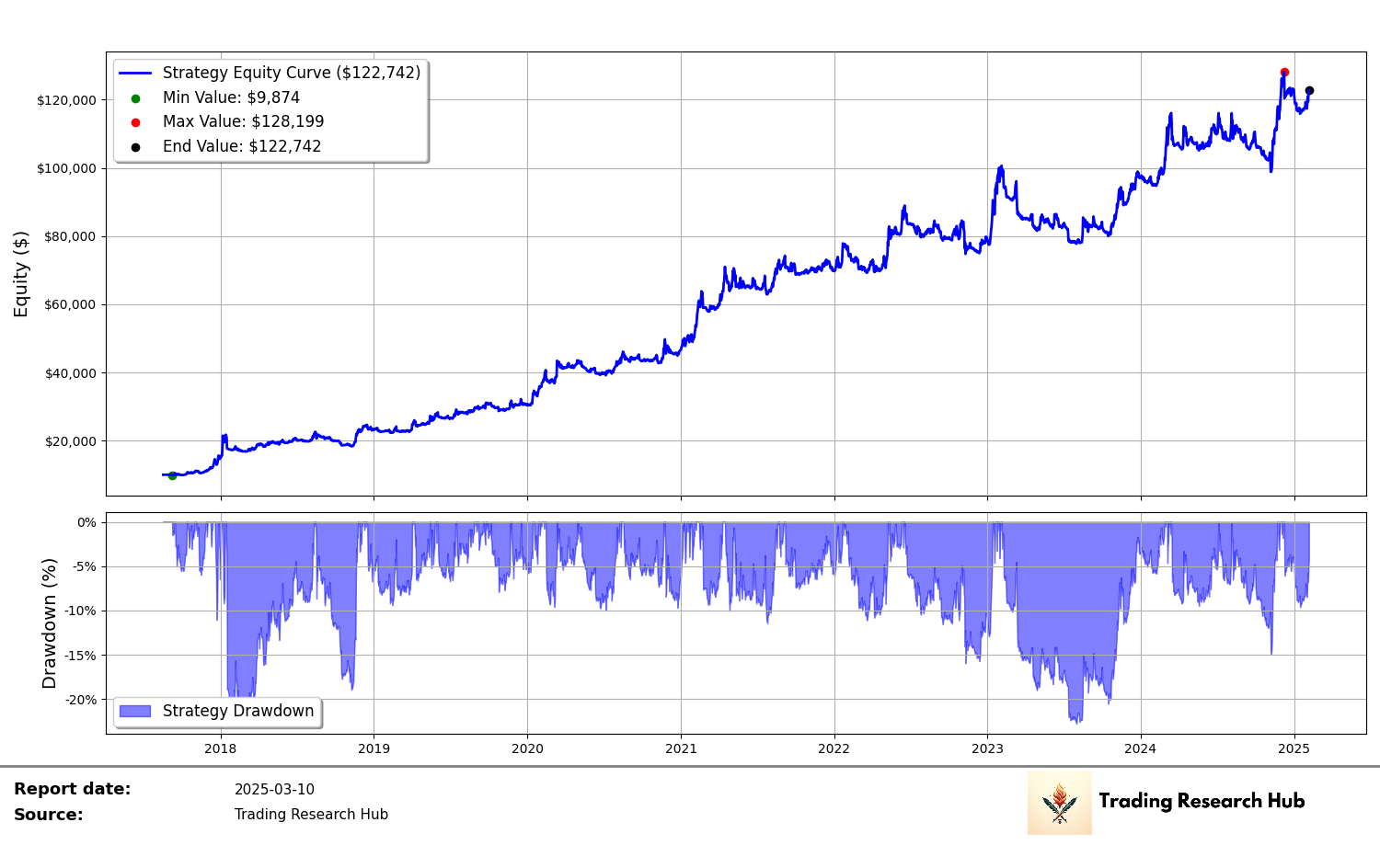

This is what we were able to achieve with today’s research.

Let’s dig into the details!

Table of Contents

Introduction

Strategy Thesis

Continuous Signal Approach

Data and Methodology

Performance Analysis

Conclusion