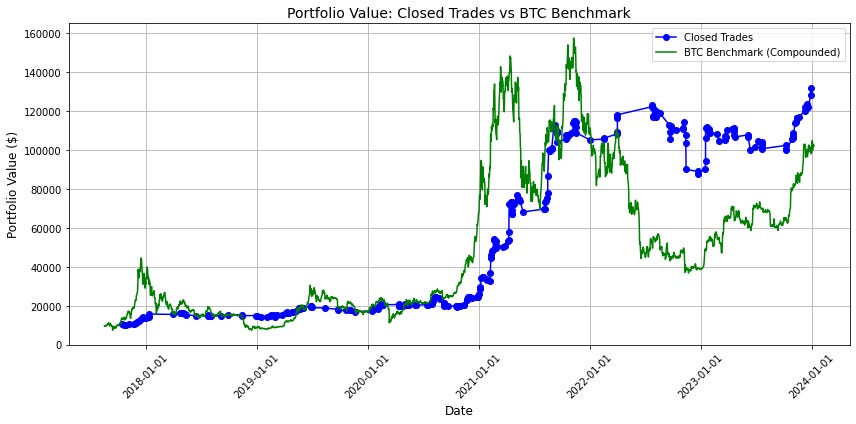

Research Article #22 - Short-Term Breakout Crypto Trading Strategy - $121,950 Total Returns

Exploring and Evaluating Cryptocurrency Trading Strategies: A Comprehensive Series

👋 Hey there, Pedma here! Welcome to the 🔒 exclusive subscriber edition 🔒 of Trading Research Hub’s Newsletter. Each week, in this series, I share my personal trading experiences and journey, offering you the behind the scenes into how I manage my own portfolios, my trading performance, new research for trading strategies and general content aimed at helping traders with the experience I’ve accumulated for the past 6 years.

My mission is full transparency by building a public track record of my performance. As I navigate through the markets, I'll be sharing every step of the journey – the ups, the downs, and everything in between. It's not just about trading; it's about growing together as a community.

Introduction

This morning, as I was drinking my coffee, I began contemplating what to write that would be most interesting to you, the subscriber of this newsletter. As previously mentioned, I aim to provide the greatest value for every dollar you spend on your subscription.

I like data. Every decision I make must be backed by some degree of data. So, I reviewed my most engaged tweets from last year and noticed a consistent theme: people enjoyed the series on the research backtests I conducted. This involved taking trading strategies from other markets and applying them to crypto. Let's do it again.

I'm considering the following structure:

A new research article every Sunday featuring a brand-new strategy.

Monthly reports on their performance.

Potential future deployment in a portfolio of strategies, with the track record made publicly available.

I believe this is an interesting idea, and I don't see many people willing to do this consistently. I'm not sure if it will work, but I'll rely on your feedback, the reader. Let's start with today's article!

By the end of this article, you will receive:

Trading Rules

All Performance Metrics

Python Code for the Backtest

The Strategy